src="http://www.1profitring.com/webring.php?u=profitline66">

src="http://www.1profitring.com/webring.php?u=profitline66">

— stephen Adetunji (@sundayAdebiyi1) September 18, 2017

Showing posts with label earn money online.. Show all posts

Showing posts with label earn money online.. Show all posts

Sunday, 7 June 2020

Monday, 9 September 2019

GETTING OUT OF DEBT

GETTING OUT OF DEBT

The Truth About Debt ConsolidationYou’re in deep with credit cards, student loan payments and car loans. Minimum monthly payments aren’t doing the trick to help nix your debt, and you’re flippin’ scared. Something has to change, and you’re considering debt consolidation because of the allure of one easy payment and the promise of lower interest rates.

Debt sucks. But the truth is debt consolidation loans and debt settlement companies suck even more. They don’t help you slay mammoth amounts of debt. In fact, you end up paying more and staying in debt longer because of so-called consolidation. Get the facts before you consolidate your debt or work with a settlement company.

Here are the top things you need to know before you consolidate your debt:

- Debt consolidation is a refinanced loan with extended repayment terms.

- Extended repayment terms mean you’ll be in debt longer.

- A lower interest rate isn’t always a guarantee when you consolidate.

- Debt consolidation doesn’t mean debt elimination.

- Debt consolidation is different from debt settlement. Both can scam you out of thousands of dollars.

What Is Debt Consolidation?

Debt consolidation is the combination of several unsecured debts—payday loans, credit cards, medical bills—into one monthly bill with the illusion of a lower interest rate, lower monthly payment and simplified debt-relief plan.

Get a FREE customized plan for your money in 3 minutes!

But here’s the deal: Debt consolidation promises one thing but delivers another. That’s why dishonest companies that promote too-good-to-be-true debt-relief programs continue to rank as the top consumer complaint received by the Federal Trade Commission.1

Here’s why you should skip debt consolidation and opt instead to follow a plan that helps you actually win with money:

When you consolidate, there’s no guarantee your interest rate will be lower.

The debt consolidation loan interest rate is usually set at the discretion of the lender or creditor and depends on your past payment behavior and credit score.

Even if you qualify for a loan with low interest, there’s no guarantee the rate will stay low. But let’s be honest: Your interest rate isn’t the main problem. Your spending habits are the problem.

Lower interest rates on debt consolidation loans can change.

This specifically applies to consolidating debt through credit card balance transfers. The enticingly low interest rate is usually an introductory promotion and applies for a certain period of time only. The rate will eventually go up.

Be on guard for “special” low-interest deals before or after the holidays. Some companies know holiday shoppers who don’t stick to a budget tend to overspend then panic when the bills start coming in.

And other loan companies will hook you with a low interest rate then inflate the interest rate over time, leaving you with more debt!

Consolidating your bills means you’ll be in debt longer.

In almost every case, you’ll have lower payments because the term of your loan is prolonged. Extended terms mean extended payments. No thanks! Your goal should be to get out of debt as fast as you can!

Debt consolidation doesn’t mean debt elimination.

You are only restructuring your debt, not eliminating it. You don’t need debt rearrangement—you need debt reformation.

Your behavior with money doesn’t change.

Most of the time, after someone consolidates their debt, the debt grows back. Why? They don’t have a game plan to pay cash and spend less. In other words, they haven’t established good money habits for staying out of debt and building wealth. Their behavior hasn’t changed, so it’s extremely likely they will go right back into debt.

How Does Debt Consolidation Really Work?

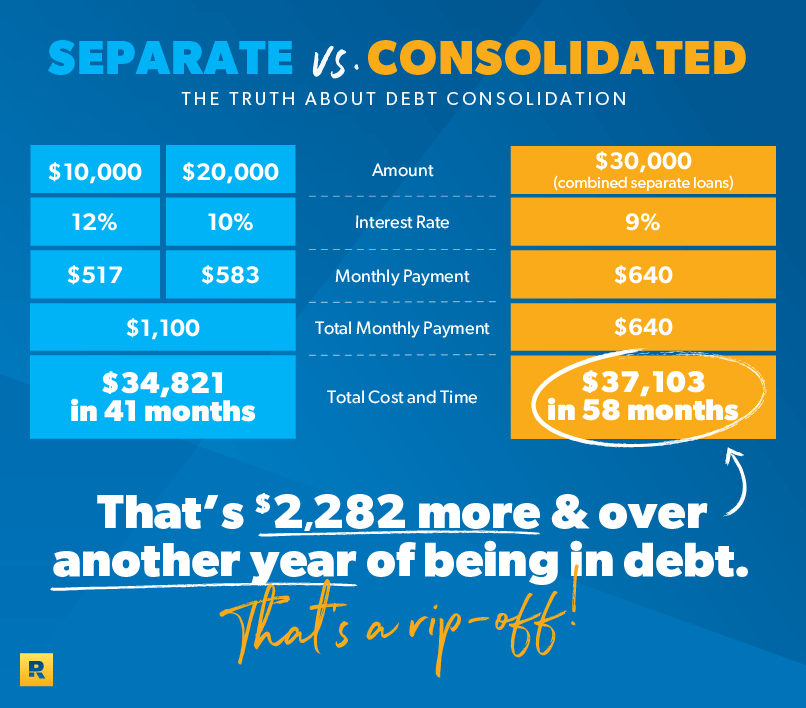

Let’s say you have $30,000 in unsecured debt—think credit cards, car loans and medical bills. The debt includes a two-year loan for $10,000 at 12% and a four-year loan for $20,000 at 10%.

Your monthly payment on the first loan is $517, and the payment on the second is $583. That’s a total payment of $1,100 per month. If you make monthly payments on them, you will be out of debt in 41 months and have paid a total of $34,821.

You consult a company that promises to lower your payment to $640 per month and your interest rate to 9% by negotiating with your creditors and rolling the two loans together into one. Sounds great, doesn’t it? Who wouldn’t want to pay $460 less per month in payments?

But here’s the downside: It will now take you 58 months to pay off the loan. And now the total loan amount would jump to $37,103.

So, that means you shelled out $2,282 more to pay off the new loan—even with the lower interest rate of 9%. This means your "lower payment" has cost thousands more. Two words for you: Rip. Off.

Credit card debt eating your lunch? Get those payments out of your life for good!

What’s the Difference Between Debt Consolidation and Debt Settlement?

There’s a huge difference between debt consolidation and debt settlement, although often the terms are used interchangeably. Pay attention here, because these crafty companies will stick it to you if you’re not careful.

We’ve already covered consolidation: It’s a type of loan that rolls several unsecured debts into one single bill. Debt settlement is different. Debt settlement means you hire a company to negotiate a lump-sum payment with your creditors for less than what you owe.

Debt settlement companies also charge a fee for their "service." Often, the fee is anywhere from 15–20% of your debt.

Think about it this way: If you owe $50,000, your settlement fees would range from $7,500–10,000. So basically, your debt would go from $50,000 to $57,000–60,000.

If that’s not bad enough, fraudulent debt settlement companies often tell customers to stop making payments on their debts and instead pay the company. Once their fee is accounted for, they promise to negotiate with your creditors and settle your debts.

Sounds great, right? Well, the debt settlement companies usually don’t deliver on helping you with your debt after they take your money. They’ll leave you on the hook for late fees and additional interest payments on debt they promised to help you pay!

Debt settlement is a scam, and any debt relief company that charges you before they actually settle or reduce your debt is in violation of the Federal Trade Commission.2 Avoid debt settlement companies at all costs.

The Fastest Way to Get Out of Debt

When you consolidate your debts or work with a debt settlement company, you’ll only treat the symptoms of your money problems and never get to the core of why you have issues in the first place.

You don’t need to consolidate your bills—you need to pay them off. To do that, you have to change the way you view debt!

Dave says, "Personal finance is 80% behavior and only 20% head knowledge." Even though your choices landed you in a pile of debt, you have the power to work your way out! You just need the right plan.

The solution isn’t a quick fix, and it won’t come in the form of a better interest rate, another loan or debt settlement. The solution requires you to roll up your sleeves, make a plan for your money, and take action! What’s the reward for your hard work? Becoming debt-free!http://charitydonor.blogspot.com/2019/06/maroon-5-donate-500k-ahead-of-super_27.html View

Monday, 26 September 2016

Proven Ways To Make Money On The Internet.

PROVEN WAYS TO MAKE MONEY ON THE INTERNET.

Sounds interesting? It will be more interesting as you read.

I am going to approach this topic from a totally different angle, as I always do. If you find this article confusing, just keep reading. You will get a clearer picture when I put everything together.

Ok, let’s start with the first proven way……

Proven Way #1 – The easiest way to make money on the internet

Do you want to know what is the easiest way to make money online?

It’s to exchange your time for money.

In other words, you make money by trading your time.

For example, you can sign up as a freelancer at elance.com and provide freelancing job to people who need your service. You can also sign up with surveying firms to get paid doing market surveys, or become a mystery shopper to help companies to do market research. If you are good in graphic design, you can also start your own online design company to provide graphic design services.

Trading your time for money is the most basic way to make money. It is also the easiest way to start making money. That’s why most people start with a ‘job’ when they are newly out from school. I hope you can see that a job is just another way to trade time for money.

There is nothing wrong to trade your time for money. In fact, if you are pressed for cash, providing online services, such as freelance services, is probably the best option to start.

Proven Way #2 – The toughest way to make money on the internet

The second proven way to make money online is to exchange your skills for money.

For example, Adsense and affiliate marketing are proven ways to make money on the internet, but you need the skills of search engine optimization, website building, PPC advertising etc before you can make money from these methods.

It is the toughest way to make money because if you do not have the necessary skills, you will have to learn. Learning new skills is ‘tough’ to most people. If you enjoy learning new skills, I’m happy for you. You will be successful soon.

Proven Way #3 – The smartest way to make money on the internet

The third way and also the smartest way is to exchange your idea for money.

The world may be changing everyday, but certain fundamentals will never change. The economy is always looking for means of doing or producing things better, faster, easier and cheaper.

If you can come out with an online idea that can do or produce something better, faster, easier and/or cheaper, you will have your fortune at your fingertips.

Now that you’ve learnt the 3 proven ways to make money on the internet, how about the one and only proven way to LOSE money online?

The Proven Way To Lose Money Online

The proven way to lose money online is to use money to make money.

If you believe that you can make $X and all you have to do is invest $Y, then you are destined to be the victim of the next online scam.

Without time, skill and/or idea, money is useless. Read again!

Don’t get me wrong. Having money will definitely help you to make more money online faster, but it is only true if you use it to buy time, skill and/or idea.

When you outsource your work to freelancers or professional services, you are buying other people’s time and skills.

When you buy into other business opportunities, you are buying the idea.

Do you see what I mean?

Summing up……

In a nutshell, you can either use time, skill and/or idea to make money online. These are the 3 proven ways to make money on the internet. I personally guarantee that. People who fail to make money online are those who refuse to invest time, refuse to learn the skills and refuse to think.

Subscribe to:

Posts (Atom)